What is Medicare IRMAA for high income earners?

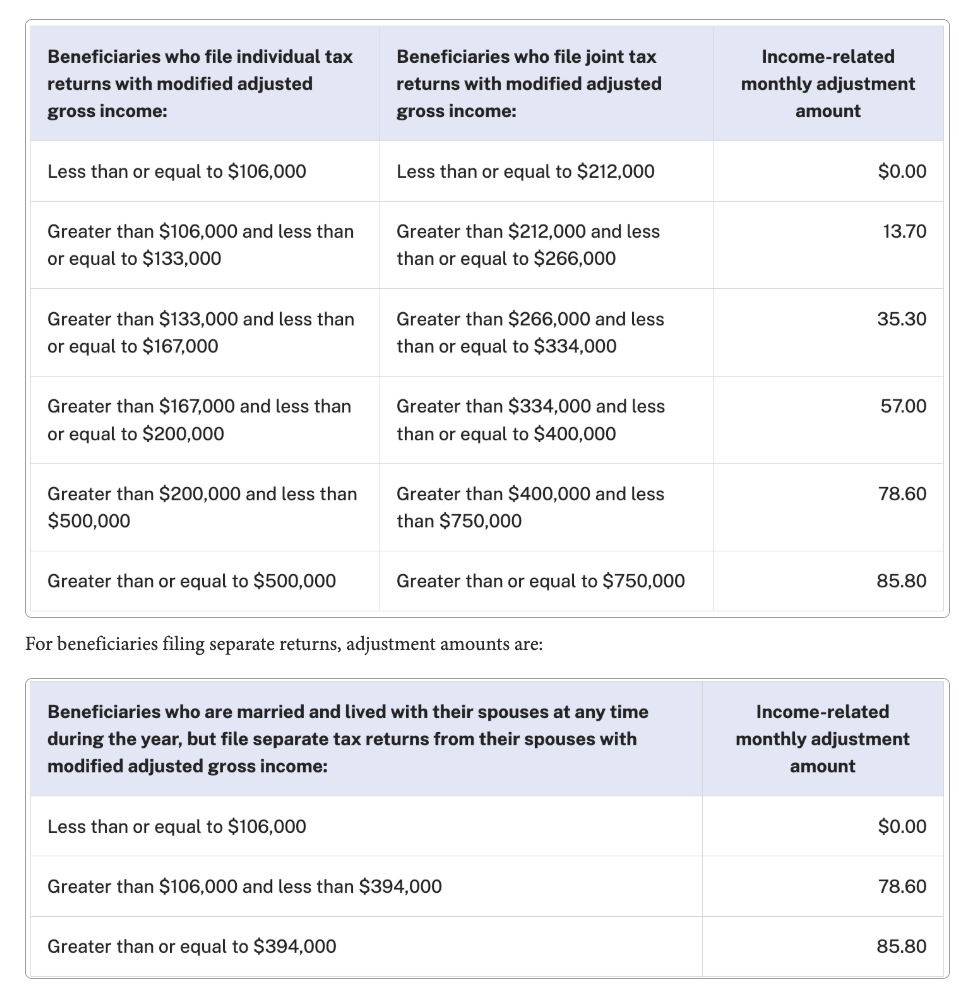

Medicare IRMAA stands for Income Related Monthly Adjustment Amount and the Social Security Administration (SSA) determines who pays an IRMAA. It is a payment that high-income earners must pay when they sign up for Medicare Part B and/or Part D plan coverage. This payment is based on the individual’s modified adjusted gross income (MAGI) reported on their most recent tax return. For those who have MAGI above certain thresholds, Medicare will charge them an additional Premium based on their filing status and income level.

The additional premiums can range from 35% to 85% of the standard premium amounts depending on the individual’s income level. Individuals with higher incomes may also be subject to a Medicare High Income Surcharge, which can add an additional 15% to the IRMAA amount they are already paying.

How is Medicare IRMAA calculated?

IRMAA, is a surcharge applied to Medicare Part B and Part D monthly premiums. Your IRMAA determination is made by the income level of the beneficiary, as reported on their most recent tax return. The IRS provides a chart each year that indicates how much the surcharge will be based on income level. Generally, those in higher income brackets receive a larger surcharge. Medicare uses an individual’s modified adjusted gross income (MAGI) to determine whether they qualify for IRMAA and how much it will be.

MAGI includes wages, taxable interest, dividends, capital gains, rental and royalty income, retirement distributions and pensions. If individuals find themselves in a higher tax bracket than expected when their IRMAA is calculated, they can request an adjustment if their circumstances have changed due to retirement or other life changes.

How much are IRMAA Part B premiums?

The cost of the IRMAA Part B premiums are determined by the income reported for the second-most recent tax year (two years prior). In other words, it’s based on your tax return two years ago. The amount can vary substantially depending on your income. Those with incomes over certain thresholds may also have to pay an additional income-related monthly adjustment amount (IRMAA) on top of their Part B Medicare premiums. For about 7% of people with Medicare Part B that have a high income, their Part B premiums can range from $230.80-$560.50 per month.

How much is the Part D IRMAA surcharge?

How do I pay the IRMAA?

Payment for the IRMAA is usually paid automatically. If you have to pay IRMAA, it will be automatically withheld from your Social Security check, Railroad Retirement Board check, or Office of Personnel Management payment. If you aren’t drawing Social Security yet, or the monthly payment is large enough to cover it, you will receive a bill from Medicare.

I have Medicare Advantage, do I need to pay IRMAA?

Unfortunately, even if you’re enrolled in a Medicare Advantage plan, you are still subject to the Medicare Part B premium as well as any additional IRMAA surcharges. You will not be able to avoid IRMAA if you purchase an MAPD plan. It’s also true, even if you obtain a $0 premium plan. If you have a Medicare Advantage plan that includes Prescription Drug Coverage (MAPD), you will still get charged for Medicare Part B IRMAA and a Medicare Part D IRMAA.

Can I appeal the IRMAA decision?

Yes you have a right to appeal an IRMAA determination if you feel it isn’t correct. You can even appeal the IRMAA ruling on a redetermination request. You can call the Social Security Administration (SSA) to request that your initial IRMAA assessment be reconsidered by phone by calling 800-772-1213 or by submitting a written request.

To qualify for a change to a determination, you need to show that your tax return was either inaccurate because of one of the following reasons specified on HHS.gov.

- The IRS data contained an error.

- The IRS sent old data and you’d like them to use newer information.

- A beneficiary filed an amended tax return for the year the Social Security Administration (SSA) used to make the IRMAA decision.

- Recent income has decreased significantly due to a life-changing event: Loss or reduction of work, marriage, annulment or divorce, death of spouse, loss of income from income-generating property, and reduction or loss of certain types of pension income. You may attempt a redetermination with the Social Security Administration using Form SSA-44.

Income Related Monthly Adjustment Amount- Final thoughts

SSA determines if you owe an IRMAA based on the income you reported on your IRS tax return from 2 years ago. If you believe your circumstances have changed or your IRMAA was miscalculated, you have the right to request that SSA lower (or eliminate) this payment increase. If you appeal SSA’s original determination, you will have to submit evidence about the original determination or if you are requesting a brand new determination.

💡 Your next step: High-income beneficiaries paying IRMAA often find that a Medicare Supplement Plan G still outperforms Medicare Advantage, with no network restrictions.

Related Articles

Written by Michael Quinn

Licensed Broker, REMEDIGAP Founder

Fact Checked by Joann Quinn

Chief Compliance Officer

As a licensed insurance broker, REMEDIGAP upholds the principles of integrity in our editorial standards and ensures transparency in how we receive compensation from our insurance partners.