When to sign up for Medicare Benefits

Enrolling in Medicare shouldn’t be stressful. However, there are many people who are completely overwhelmed by the process. And, one of the most common areas of concern is Medicare enrollment. It’s likely you’ll receive tons of mail about Medicare insurance. But, highly unlikely that any of it will inform you about when to sign up for Medicare benefits.

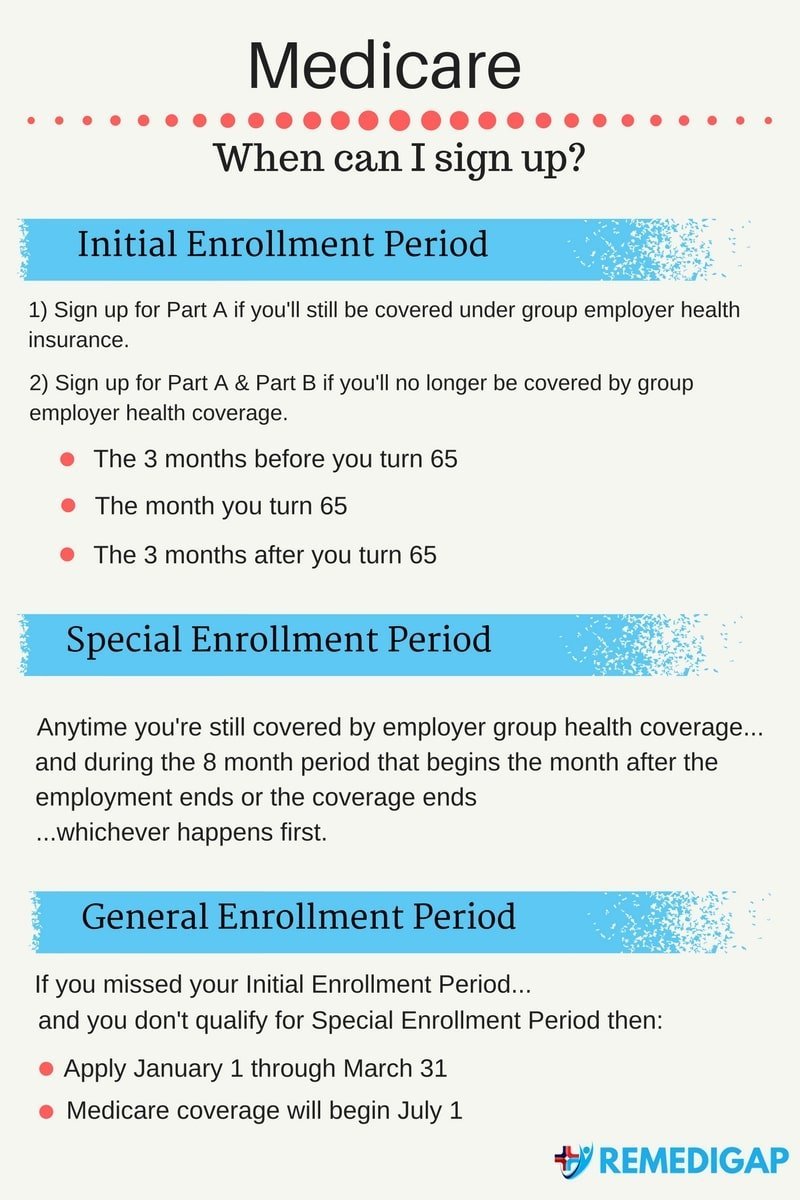

When should you sign up for Medicare benefits?

Before I answer the question about when to sign up for Medicare benefits, let me assure you that enrolling in Medicare and understanding how it works doesn’t have to be complicated. I’ll show you how easy it is to figure out when to sign up for Medicare benefits. Keep in mind, there are three Medicare enrollment opportunities and it’s important to know which one(s) apply to you.

Signing up for Medicare when you’re first eligible

The most common time for people to sign up for Medicare is during the Initial Enrollment Period. It applies to anyone turning 65 years young. If you plan on retiring and you’re not going to have employer group health coverage, then this is the time to apply for Medicare Part A and Medicare Part B.

Free Tool: Use our Medicare Enrollment Calculator to help you find out your Medicare enrollment deadline.

The Initial Enrollment Period lasts for 7 months. It begins 3 months before your birthday month. It includes your birthday month and the 3 months after. If you sign up for Medicare during the 3 months before your 65th birthday month, in most cases, your coverage starts the first day of your birthday month.

However, if your birthday is the first day of the month, your coverage will start the first day of the prior month. So, if your birthday is May 1, your Medicare coverage will start on the 1st day of April.

But, if your birthday is anywhere between the 2nd through the last day of the month, your coverage will begin on the first day of that month. For example, a birthday on May 17 will result in an effective date of May 1.

Sign up for the best Medicare start date

When to sign up for Medicare benefits is extremely important when choosing a start date.

Now, if you enroll in Medicare during your birthday month or the 3 months after, your start date for Medicare coverage will be delayed.

So, if you want Medicare coverage to begin on the first day of your birthday month, then sign up for Medicare during the first 3 months of your Initial Enrollment Period.

When to sign up for Medicare benefits if you or your spouse will continue working

There’s a growing population who continue to work beyond retirement age. If you or your spouse will continue working and you keep the group employer health insurance, then you should consider delaying Medicare Part B.

Why delay enrolling in Part B?

Medicare Part B is medical insurance. In most cases, if you have group employer health insurance, you may not need to sign up for Part B.

Remember, you have to pay a Premium when you sign up for Part B. That’s why many people under group employer health coverage delay Part B enrollment. With that said, it’s highly recommended that you check with your employer Benefits Administrator to make sure their coverage is as good or better than Medicare.

It’s important to note that if you delay Part B, you can still sign up for Part A during your Initial Enrollment Period. Your employer group health coverage will work with Medicare, but there are rules about which insurance pays first.

You can find out who pays first and how Medicare coordinates with other coverage here: Medicare.gov | Which insurance pays first

You won’t be penalized for delaying Part B as long as you have continuous group employer health coverage. Once that ends, most people have an opportunity to sign up for Part B through the Special Enrollment Period.

The Special Enrollment period applies if…

…you or your spouse are still working and you don’t sign up for Part B (or A if you have to buy it) when you’re first eligible because you’re covered under a Group health plan based on employment.

It allows you to sign up for Part B (or Part A if you have to buy it) anytime you’re still covered by employer group health coverage. The Special Enrollment Period is an 8 month window that begins the month after the employment ends or the coverage ends, whichever happens first.

Signing up for Medicare when COBRA and Retiree Health Plan Ends

Unfortunately, COBRA and retiree health plans aren’t considered coverage based on current employment. So, you aren’t eligible for a Special Enrollment Period when that coverage ends.

So, keep that in mind and consider signing up for Medicare when you’re first eligible. Otherwise, you may be subject to an enrollment Penalty.

Are there any other Medicare enrollment opportunities?

Sometimes people don’t sign up for Medicare during their Initial Enrollment Period. Which means the period of time they can sign up for Medicare becomes limited.

If you miss the Initial Enrollment Period and don’t qualify for the Special Enrollment Period, you can sign up for Medicare between January 1 and March 31. This period of time is known as the General Enrollment Period.

BUT BEWARE! Your coverage won’t start until July 1st of that year. It’s also possible that you’ll be penalized for signing up late.

When’s the best time to sign up for Medicare Benefits?

1) If you’re signing up for both Part A and Part B, apply for Medicare once your Initial Enrollment Period starts. This will allow you plenty of time to get your Medicare card before your 65th birthday month.

2) Most people apply for Part A during their Initial Enrollment Period if they plan on keeping group employer health coverage. Then they apply for Part B during the Special Enrollment Period. Ideally, it’s best to coordinate Medicare to start immediately after your group employer health coverage ends.

3) If you have Medicare because of a disability or receive Social Security benefits, you’re automatically enrolled in Part A and Part B.

About REMEDIGAP

Thank you for reading our article “When to Sign Up for Medicare Benefits?” . At REMEDIGAP, we strive to provide the tools you need to make informed decisions about your Medicare benefits. Our video page, blog articles and Facebook Page are full of valuable information to help you make important decisions about your Medicare coverage.

In addition, we’ve created a Medicare eCourse where you receive one email a day for a week. Each email covers important topics about Medicare and Medigap insurance. Most importantly the eCourse is designed to make Medicare less confusing.

Sign up for the eCourse here ====> www.remedigap.com/ecourse

As you learn about Medicare, you may have many questions or none at all. Either way, we customize our approach based on your needs. Most importantly, our service is free to everyone!

In full transparency, independent insurance agents are compensated by insurance companies based on a policy commission schedule. It’s not standard procedure for an insurance agent to charge a consultation fee. If an insurance professional is asking you to pay for information, you should consider looking for a new agent.

So what are you waiting for? Just give us a call at 888-411-1329 or simply click on our quote form for free Medigap quotes. It’s an easy way to see just what we can do for you!

💡 Your next step: Your Medicare enrollment window is the best time to get Medigap — no medical Underwriting required. Compare Medicare Supplement plans before your window closes.

Related Articles

Written by Michael Quinn

Licensed Broker, REMEDIGAP Founder

Fact Checked by Joann Quinn

Chief Compliance Officer

As a licensed insurance broker, REMEDIGAP upholds the principles of integrity in our editorial standards and ensures transparency in how we receive compensation from our insurance partners.