Switching Medigap Plans – Can you change plans and companies?

can you change Medigap plans?

Perhaps you bought a Medigap plan and had a low Premium initially. But now the rate seems a little high compared to the original premium. If so, you’re probably looking into switching Medigap plans. If you are still in the same Medigap Plan since your Initial Enrollment Period, then your premium could be getting a little uncomfortable. This is not uncommon as rates increase at least once a year (sometimes more). Before you know it, your one time low premium is now creeping closer to $200 a month or more.

If this sounds like your situation, continue reading to see how you can switch Medicare Supplement insurance companies and reduce your premium. You’ll also want to understand the differences about Medicare Plan N vs Plan G.

Do you want to keep your current benefits and lower your premium?

There are 10 standardized Medigap Plans (A, B, C, D, F, G, K, L, M, N). Many people have Plans F, G, or N. If you qualify medically, there’s a good chance you can lower your premium for the standardized plan you already enjoy.

Are you and your spouse willing to use different insurance companies?

If you and your spouse have Medigap Plans with the same insurance company, you may save more money by being insured by different companies.

How can you save money?

Each insurance company has health questions that are unique. Medical Underwriting requirements are not standardized, so each insurance company has a different set of parameters. Since your health history may differ from your spouse, so could your ability to qualify with the same insurance company.

Here’s an example…

Let’s say, for example, that Mr. and Mrs. Client would like to replace their current Medigap Plan N.

Mr. Client had a stent put in three years ago and Mrs. Client has rheumatoid arthritis. Both can still apply for a new Medigap Plan N; however, it’s possible they may have to each get a policy with separate insurance companies because of their differing health conditions.

Each insurance company has different underwriting guidelines. That means one insurance company may look more favorably with certain health conditions vs. other conditions.

If Mr. Client can save $50 a month with ABC insurance company and Mrs. Client can save $75 a month with XYZ insurance company for the exact same Medigap Plan N, then it’s worth the savings to change Medicare Supplement insurance companies.

On occasion only one spouse will qualify medically, but that doesn’t mean you can’t take advantage of savings. It’s okay if one person moves to a new insurance company and the other person stays with the current company. Especially, if it means you’ll be keeping more of your money.

The unknown is scary and the thought of switching Medigap insurance companies overwhelms some people. I’ve spoken with couples who would rather just keep paying more money so they can both stay with the same insurance company.

Does this sound like you?

In reality, if you both have Medigap Plan F then you both have the exact same benefits (just a different ID card).

It’s the long term effect of keeping dollars in your pocket that’s most important…not what insurance company is on your ID card, wouldn’t you agree?

Do you want more benefits?

After using your Medigap plan for sometime, perhaps you’ve realized the need for more benefits. A common complaint I hear is about how annoying it is to receive medical bills when you have a Medicare Supplement plan.

The only Medigap Plan where all Medicare eligible charges are paid is Medigap Plan F.

If you have any of the other 9 standardized Medigap Plans (A, B, C, D, G, K, L, M, N), you may be subjected to the following charges.

- Part A Deductible

- Part B Deductible

- Excess charges

- Co-insurance

- Co-payments

More benefits may also mean higher premiums

If you already have a plan, you might be able to replace it with one richer in benefits for about the same premium or less.

I spoke with Ms. G in Kentucky who had a Hi-Plan F. Her premium was $109 a month…which is really high for this type of Medigap Plan. The Hi-F Plan is actually a high Deductible Plan F. This means that you are responsible for paying an annual deductible of $2,180 (in 2016) before your plan pays anything.

The problem with Ms. G’s Hi-Plan F was that her premium was double what it should be. In fact, she was paying an extra $68 a month to keep it with her original insurance company. For the same Hi-Plan F benefits, she could switch to a different Medigap insurance company and pay $41 a month instead of $109.

If she wanted more benefits, she could change to Plan G and drastically lower her annual deductible. Her new rate would be $106 a month. Just a few dollars less than her original $109 premium.

Another example of needing extra benefits can be represented through Medigap Plan N. If you have Medigap Plan N, then you probably get some bills for different medical procedures. With Plan N, you are responsible for the annual Part B deductible, co-pays and excess charges.

The lure for Plan N is the fantastic premium. However, if you’d had Plan N for some time, the premium may not be so fantastic anymore.

As with all premiums, your Medigap Plan N rate increases every year. If you purchased from one of the major insurance companies, I’m willing to bet you are overpaying for your Medigap benefits. In fact, you may be able to get more benefits for about the same price or even less.

Do you need less benefits?

It’s very rare that someone wants fewer benefits. However, when their Medigap Plan F premium has skyrocketed, they become more open to a Medigap Plan with fewer benefits.

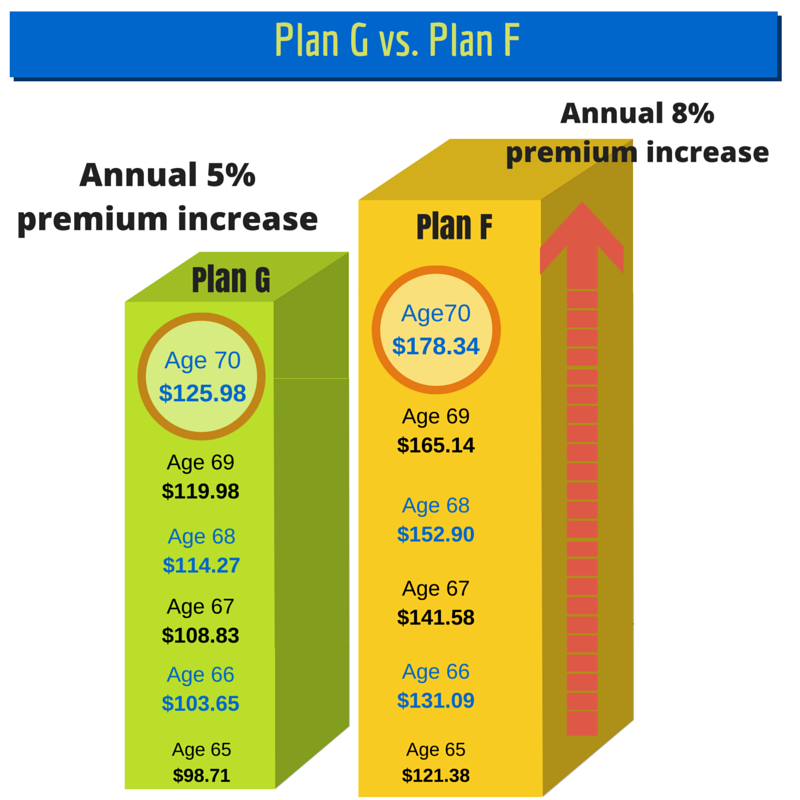

Most often it is Medigap Plan G that makes the most sense when it comes to “less benefits”. Medigap Plan G compared to Medigap Plan F is not much different. The benefit you lose with Plan G is the coverage for the annual Part B deductible.

After the Part B deductible is met, Medigap Plan G works just like Medigap Plan F. However, paying the Part B deductible yourself can reap great savings over the long run.

when can you change medigap plans?

If you are not in a Guaranteed issue situation or still in the Initial Enrollment Period, then you will have to qualify medically. This means the insurance company will ask you some health questions on the application, verify your prescriptions, and possibly conduct a phone interview with you.

After the phone interview, the application is reviewed in the medical underwriting department to determine your acceptance.

Do you have any health issues?

Each insurance company has a unique set of health questions. You might be surprised to know that you may qualify for a Medigap Plan with the following health conditions:

- Diabetes

- Heart incidents that occurred two years ago or longer

- COPD

- Osteoporosis without fractures

- Rheumatoid arthritis

Thank you for reading our post on changing Medicare Supplemental plans. Switching Medicare Supplement plans can allow you to save money and still get the same great benefits.

About REMEDIGAP

We proudly customize our approach to your fit your needs. We can answer all your questions and educate you on Medigap through email or by phone. It’s your choice. We don’t like being hassled by sales agents, so we know how it feels to avoid those situations. We don’t ever feel comfortable pressuring anyone to buy from us. We offer you the information and let you make the decision that suits you best.

Contact us today through any of the choices below:

- Call 888-411-1329

- Complete our Quote request form on this page

- Comment below

- Email us

Additional Resources:

Related Articles

- Medicare Plan G

- Are Medicare Supplement Plans Worth It?

- AT&T Retiree Health Insurance – Your Medicare Options

- Compare Supplemental Medicare Insurance Rates

- GE Retirees Can Get Better Medicare Supplement Options

Medicare Supplement Plans

Written by Michael Quinn

Licensed Broker, REMEDIGAP Founder

Fact Checked by Joann Quinn

Chief Compliance Officer

As a licensed insurance broker, REMEDIGAP upholds the principles of integrity in our editorial standards and ensures transparency in how we receive compensation from our insurance partners.